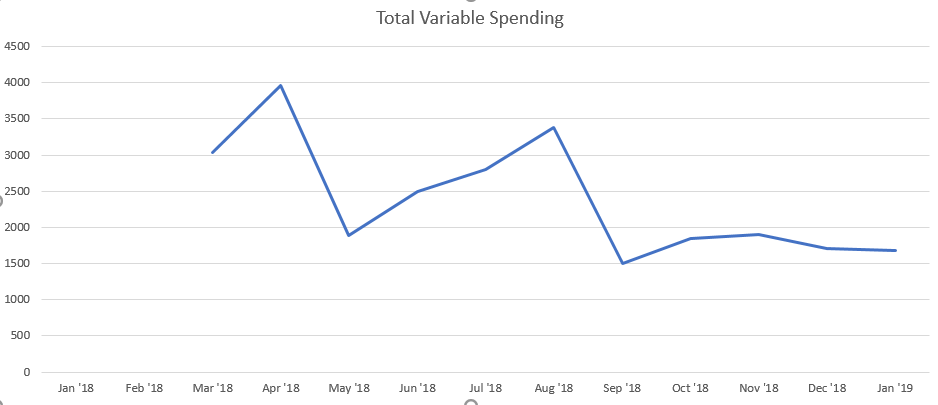

Fixed spending down because of a lack of Council Tax, variable spending up because of replacement car tyres following an MOT.

Overall, happy with the consistency though and recording our 6th straight month of spending less than we earnt.

Spending levels are in line with previous years so far.

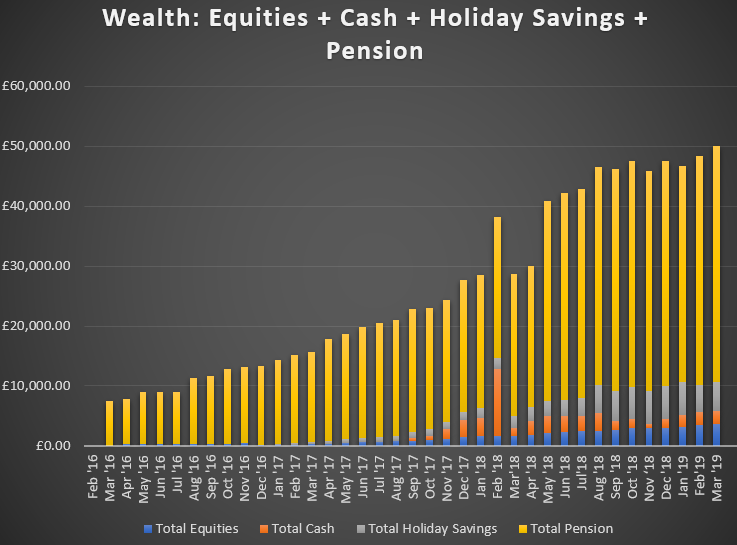

Total wealth topped £50k for the first time.

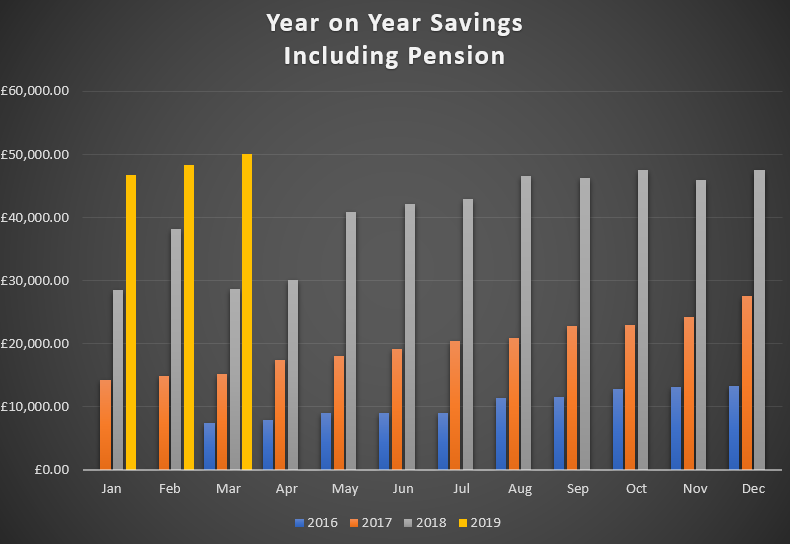

Difference between what we owe (exc Mortgage) and our savings (exc Pension and exc our holiday savings) increased very slightly again. Expecting to see a much more significant change in this next month.

Finally, it's always good to see how far we have come in terms of our savings including pension in the last few short years.

And then very sobering to see how much we actually owe compared to this...