So, did we stick to the budget?

No. Overspent by £314.55.

Holiday. Actually I expected to spent a lot more.

The aim was to maintain the downward trajectory on the monthly overspend. The graph above shows we succeeded with this.

Any positives?

Kept spending lower than I expected.

Grocery shopping was £120 less than budgeted. Our third on-budget or better month in a row. Previously this had been a big killer.

Lessons / thoughts?

Nowt this month.

Expectations for next month?

Nowt this month.

Expectations for next month?

Really struggling to think of things which we'll be spending money on next month. Something almost always comes up but really hoping can stick to our budget.

Effect on overall finances?

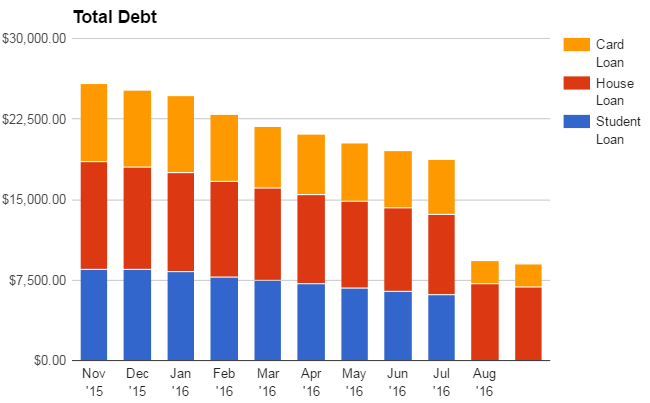

S Student loan – Does not exist anymore :)

· House loan – £298 was paid off direct debit. Total remaining now is £6,249

· Credit Card - £47.58 was paid off. Total remaining now is £2,067.34

Total Debt = £8,316

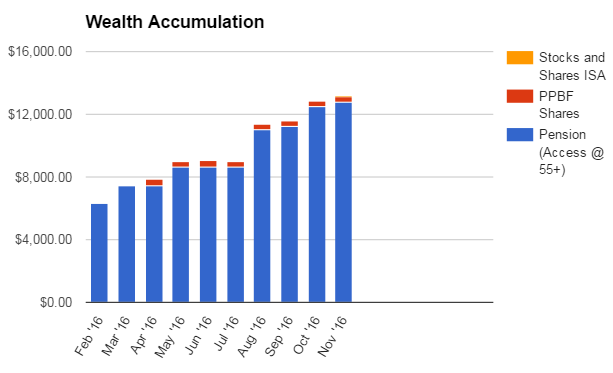

Wealth Accumulation

Summary:

Finally opened up a global index tracker fund. Starting with £50 per month direct debit into this. As mentioned in previous post depending upon the outcome of our house move this may increase or not.

It feels like a big thing beginning.

PPBF shares continued negative trend.

Next month will get the first entry for my workplace sharesave scheme = £100 per month into that.

Noticed that we've now doubled our positive saved wealth in the 9 months since February.

|

Asset |

Value

|

Month Increase

|

|

Pension Value |

£12,761.50

|

£260.95

|

|

PPBF Share |

£340.78

|

-£9.10

|

|

Cash Savings |

£0

|

n/a

|

|

Fidelity Global Index Tracker |

£50

|

£50

|

|

|

|

|

|

Total |

£13,152.28

|

£301.85

|